Last Updated: June 2026 — FY 2025-26 (AY 2026-27)

Filing your return? Read our complete NRI income tax return filing guide FY 2025-26 – residential status tests, TDS refunds, DTAA paperwork and a step-by-step ITR-2 walkthrough.

Non-Resident Indians (NRIs) have specific income tax obligations in India. Income earned or received in India is taxable, while foreign income is generally exempt.

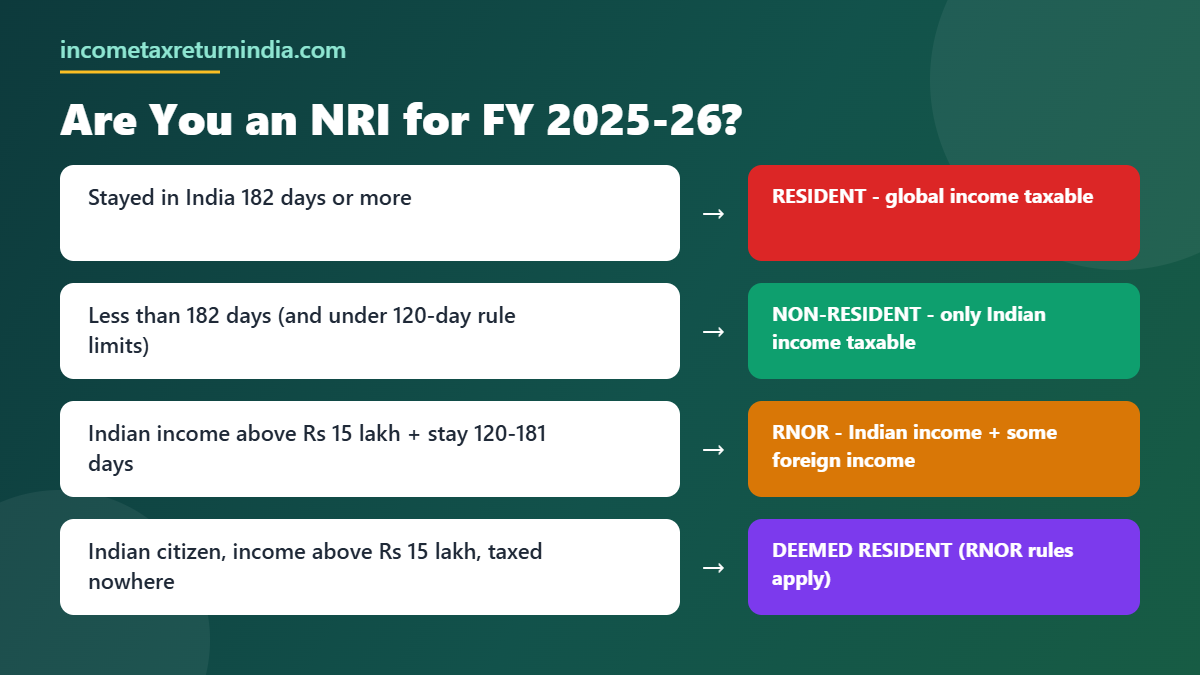

Who is an NRI for Tax Purposes?

You are an NRI for FY 2025-26 if you stayed in India for less than 182 days during the year. The RNOR (Resident but Not Ordinarily Resident) status has intermediate rules based on cumulative days over 10 years.

What Income is Taxable for NRIs?

- Salary received in India or for services in India

- Rental income from property in India

- Capital gains on assets in India (shares, property)

- Interest on NRO accounts, fixed deposits in India

- Business income from India operations

TDS Rates for NRIs (FY 2025-26)

| Income Type | TDS Rate |

|---|---|

| Short-Term Capital Gains (equity) – Sec 111A | 20% |

| Long-Term Capital Gains (equity) – Sec 112A | 12.5% |

| Long-Term Capital Gains (property) – Sec 112 | 12.5% (without indexation) |

| Interest on NRO Account | 30% |

| Rental Income | 30% |

| Other Income | 30% |

NRI – ITR Filing Requirements

- NRIs must file ITR if their India-sourced income exceeds the basic exemption limit

- No basic exemption benefit on special rate incomes (capital gains, etc.)

- NRIs can claim DTAA benefits to avoid double taxation

- Applicable ITR forms: ITR-2 (no business income) or ITR-3 (business income)

- Filing deadline: 31 July 2026

NRE vs NRO Accounts – Tax Treatment

| Account Type | Interest Taxability |

|---|---|

| NRE Account | Fully Exempt from Indian tax |

| FCNR Account | Fully Exempt from Indian tax |

| NRO Account | Taxable at 30% (TDS deducted) |

hi

I will be resident and not ordinary resident in india for the FY 2013-14. I have fixed deposits in NRE a/c in Rs which i made when i was NRI last year. Should i be taxable for interest on NRE deposits even if i am resdient and noR.

I am an NRI residing in the USA. Every year I am facing a problem of getting my refund credited to my bank acount (ECS) as I am informed that my refund amount is larger than Rs. 50,000. My house in India is not occupied and locked. I have no relative who I can entrust this work. All my sources are helpless because my refund is posted by SBI to my India address and the post intimation lies there and then the refund cheque goes back. Is there a way out for my every year problem?

I had authorised my Chartered Accountant to collect the refund for me but he is helpless because the post office refuses to give my refund envelope to him unless he produces the postal intimation.

Please help.

Thanks.

Dear sir ,

This is very useful for NRI s. I forwarded the same to my daughters

TATARAO

I am working for Dubai base company and my job is like one month in

India and one month out of India. i have an NRE account in Indian Bank, my company depositing my salary in USD in my NRE account. My question is “I have to pay TAX or Not”. Please help me.

You need to pay tax and add your both income in case your status is Resident of India.

thanks Tax dost,

i am always getting my salary in USD (India or out of india). how i can know that, my status is resident or NRI because it is my first time for working in this company. Is any online provision for this to my resident check status. My company is telling that my salary is Tax free. I am ready to pay tax (FY2013-14, AY 2014-15) but If i could not able to pay Tax before 31 June 2014 then can i pay this before 31 march 2015 without any pennalty.

I am an Indian and working in abroad. Do I need show my remmitance in ITR? If yes then under which section? How can I show my income in IT file? And who will give the income certificate?

For ex. if I apply for a loan then how they will validate my income?

Thanks,

Narendra

There is no need to show your remittance in your tax return . You only need to show income earned in India in your Tax Return.

i am NRI and resides at USA I am pensioner of SBI and they deducted tax from my pension every year, and there are some Fixed Deposite in SBI which are given by my parents for me and my brother and sister which are in my name because my brother and sister both are NRI and they doesn’t have Bank’s Account but Bank deducted TDS on them and i want to know i have to file returns of income tax in india and how can you please explain me in details.

Thanks Raju Patel

Please use Income tax form 1 and show your income from pension and interest income.

I am NRI and resides at USA. I am pensioner of AP state Gov. and they deducted tax from my pension every year. I am paying LIC premiums every year from my pension. Can LIC premiums payments be deducted from my net salary.

Sir,

You will have to file income tax return to claim LIC premium benefit under section 80C.

Hey,

I am an Australian Citizen and looking to move back to India. However, I will retain my Australian citizenship.

My question is how would I be considered for Tax purposes. And if the tax slab is same for oversees citizen as well.

Thanks

Sanjay

Your Tax status will be determined by your residential status. If you status is resident Indian, then income earned (across India+ or australia) will be taxable here in India.

I am having US and Indian Citizenship. If I invest in Insurance Policies in India, what will be the tax implications at the time of maturity. Is is taxable

Hello,

i live in USA and i have taken loan to help my family member in India. they just used my salary slip to get the loan. On paper i am the primary loan holder. but my fmaily is taking care of loan premium. As I used my USA salary slip, they want loan premium to be deducted from my NRO acct. My family is depositing loan premium amt in my NRO acct and it gets deducted by Lender bank. I came to know that whatever amt my family is depositing in my NRO acct is being treated as my income in India so I need to pay taxes on that. Is it true? Kindly reply ASAP on this. I am not getting any answer form bank on this.

Thanks.

my daughter is nri living in australia having PR status. she has investesd in birla sun life[BSLI Vision life income plan] 10000/- per month for 15 years to pay and

Edelweiss Tokio Life Gcap 15000/- per month for 7 years to pay in the month of march 2016.The returns on these policies are tax free. now my question is what will happen if my daughter opt for australinan citizenship which she will likely doing so next year ie 2017.