Filing an income tax return for F&O trading is very different from filing a salary-only return. Futures and options income is business income, which means a different ITR form (ITR-3), turnover computation, possible tax audit, and valuable loss carry-forward benefits. This step-by-step guide walks you through how to file ITR-3 for F&O trading for FY 2025-26 (AY 2026-27) – including the two big changes this year: the new 31 August 2026 due date for non-audit ITR-3 filers and the mandatory separate disclosure of F&O and intraday turnover in the new ITR-3 form.

Quick answer: F&O income is non-speculative business income, taxed at slab rates and reported in ITR-3. Compute turnover as the absolute sum of profits and losses, check the Rs 10 crore audit limit, report F&O and intraday separately in the new form, and file by 31 August 2026 to keep your 8-year loss carry-forward. New to F&O taxation? Start with our F&O trading income tax FAQ first.

Who should file ITR-3? (And when ITR-4 or ITR-2 applies)

If you traded futures or options even once during FY 2025-26 – on NSE, BSE or MCX, whether index, stock, or commodity derivatives like gold, silver and crude – you have business income and ITR-3 is your form. This applies whether you are a full-time trader or a salaried employee who trades on the side.

- ITR-3 – the default form for F&O and intraday traders. It is the only form that lets you claim actual expenses and carry forward losses.

- ITR-4 (Sugam) – only if you opt for presumptive taxation under Section 44AD (covered below).

- ITR-2 – only for investors with no business income (salary, capital gains from delivery-based investing, other sources). Reporting F&O in ITR-2 as capital gains is a common and costly mistake.

Documents you need before you start

- Broker Tax P&L statement for FY 2025-26 (Zerodha Console, Groww, Upstox, Angel One etc. all provide one) – for every broker you used

- Ledger and holding statements from each broker, plus margin balance as on 31 March 2026

- Bank statements of accounts used for trading transfers

- Form 26AS, AIS and TIS from the e-filing portal – your F&O data is reported here, so your ITR must match

- Form 16 if you also have salary income

- Capital gains statements for delivery equity and mutual funds, if any

- Expense proofs – internet bills, advisory/subscription invoices, depreciation working for laptop, etc.

See our guide on how to check Form 26AS to reconcile TDS before filing.

Step 1: Classify your trading income into the right buckets

The income tax law treats each type of market activity differently, and the new ITR-3 for AY 2026-27 forces you to disclose them separately:

| Activity | Head of income | Where in ITR-3 |

|---|---|---|

| F&O (futures & options) | Non-speculative business income | Trading Account / Schedule BP – own F&O fields |

| Intraday equity (no delivery) | Speculative business income | Schedule BP – separate speculative fields |

| Delivery shares / mutual funds | Capital gains | Schedule CG |

| Salary | Salary | Schedule S |

| Interest / dividend | Other sources | Schedule OS |

New for AY 2026-27: the revised ITR-3 has dedicated fields for F&O turnover/income and intraday turnover/income. Clubbing them together – or leaving the fields blank – can get your return marked defective under Section 139(9).

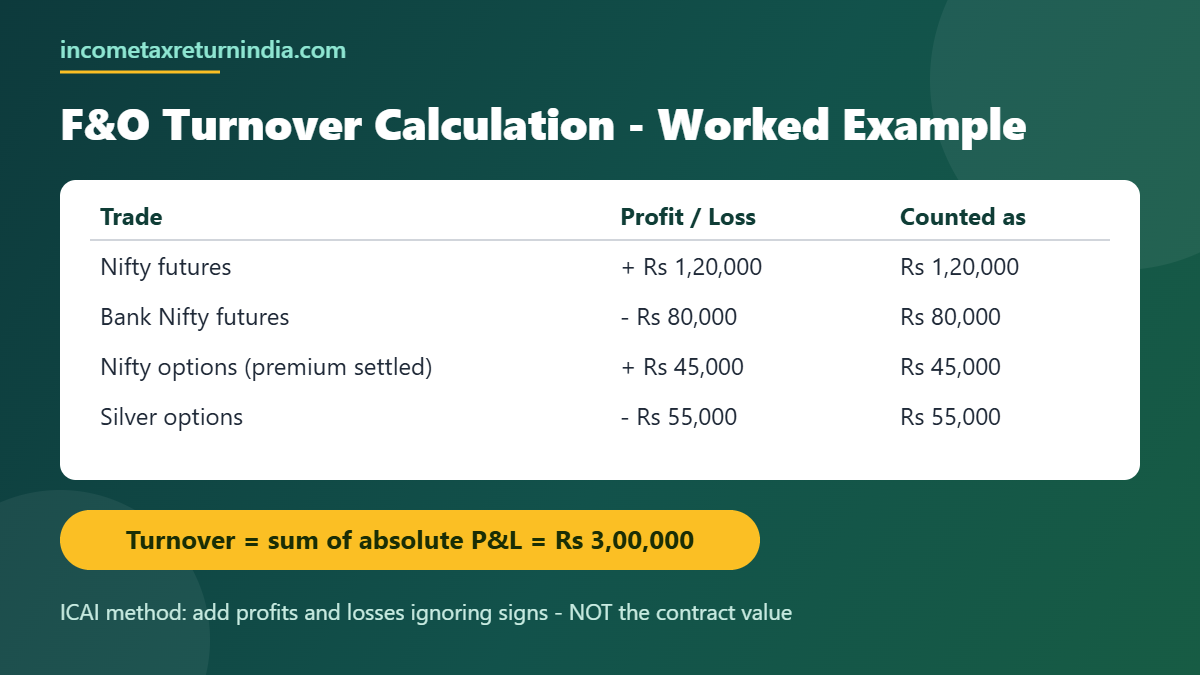

Step 2: Calculate your F&O turnover correctly

Turnover decides your audit applicability, so get this right. For F&O, turnover is not the contract value. As per the ICAI Guidance Note on Tax Audit, turnover is the absolute sum of all profits and losses – add every profit and every loss, ignoring the minus signs.

In this example the trader’s net result is a profit of just Rs 30,000, but the turnover is Rs 3,00,000. Premium received on options sold is not added separately when it is already included in the profit/loss figure. Most broker tax P&L reports compute this turnover for you – but always verify, especially if you trade with multiple brokers (turnovers of all brokers are added together).

Step 3: Do you need to maintain books of account?

Under Section 44AA, an individual must maintain books of account if business income exceeds Rs 2,50,000 or turnover exceeds Rs 25,00,000 in any of the three preceding years. Most active F&O traders cross these limits, but compliance is simple: your broker statements, bank statements and a basic Excel of expenses effectively serve as your books. In ITR-3 you will fill:

- Trading Account / P&L – F&O turnover as gross receipts, minus expenses, giving net profit

- Balance Sheet – your broker margin balance, bank balances, and capital as on 31 March 2026

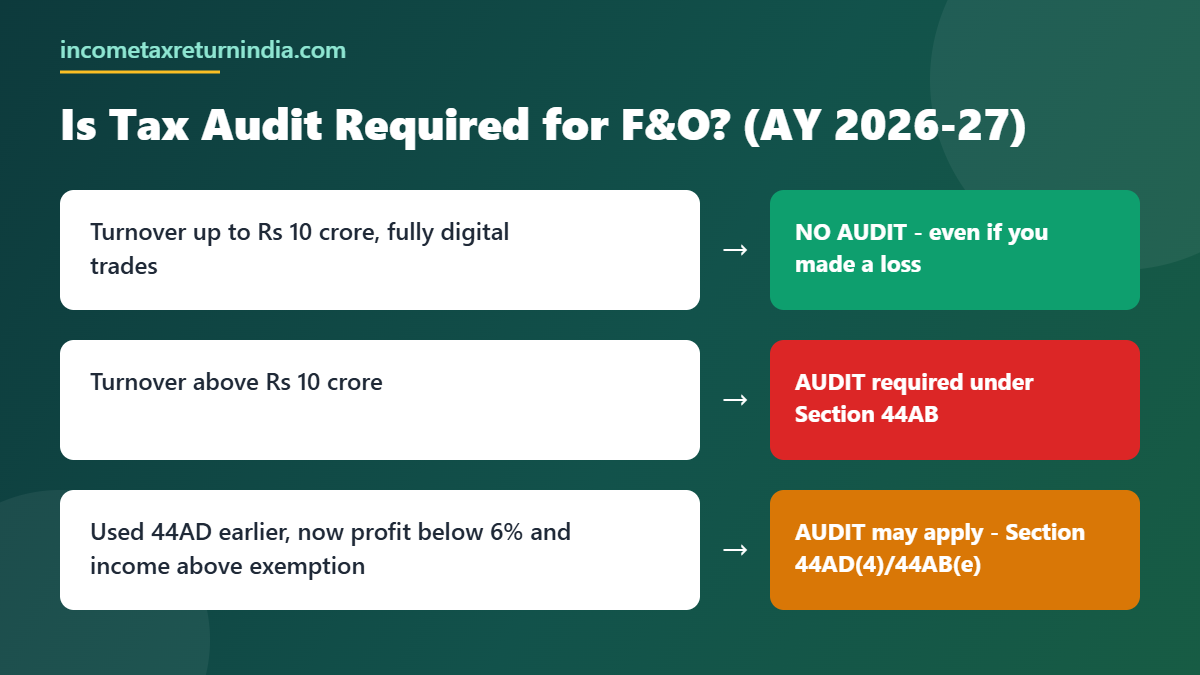

Step 4: Check whether tax audit applies to you

This is the most misunderstood area in F&O taxation. A tax audit under Section 44AB is not triggered merely because you made a loss.

- Turnover up to Rs 10 crore – no audit, provided cash receipts and cash payments are each 5% or less of totals. Since F&O trades are 100% digital, virtually every trader qualifies for the Rs 10 crore limit. No audit even if you have a loss.

- Turnover above Rs 10 crore – tax audit is mandatory. Your CA files Form 3CD, and your due date becomes 31 October 2026.

- The 44AD trap – if you opted for presumptive taxation in any of the last 5 years, then declare profit below the 6%/8% deemed rate while your total income exceeds the basic exemption limit, audit can apply under Section 44AD(4) read with 44AB(e).

Should you opt for presumptive taxation (Section 44AD)?

If your F&O turnover is up to Rs 2 crore (Rs 3 crore where at least 95% of receipts are digital), you may declare 6% of turnover as deemed profit, file ITR-4, and skip detailed books.

- Works well when: your actual profit is higher than 6% of turnover and you want minimal compliance.

- Avoid when: you have a loss or thin margins – under 44AD you cannot claim actual expenses or carry the loss forward, and opting out later can lock you out of the scheme for 5 years and trigger the audit rule above.

Most serious traders with losses or large expense claims are better off with regular ITR-3 filing. Talk to a CA before choosing – our team can run both computations for you.

Step 5: File ITR-3 on the e-filing portal – the walkthrough

- Log in at incometax.gov.in with your PAN. Go to e-File, then Income Tax Returns, then File Income Tax Return.

- Select AY 2026-27, Online mode, and choose ITR-3.

- In Personal Information, confirm your details and choose your tax regime. The new regime is the default; to use the old regime with business income you must file Form 10-IEA before the due date (and note – with business income you can switch out of the new regime only once in your lifetime).

- In Schedule Trading Account / P&L, enter F&O turnover and results in the dedicated F&O fields, and intraday figures in the separate speculative fields. Do not club them.

- Claim your trading expenses against F&O income (see the expense list below).

- Fill the Balance Sheet – broker margin balances, bank balance, capital.

- Complete Schedule CG for delivery equity/mutual fund gains (see our capital gains tax guide), Schedule S for salary, and Schedule OS for interest and dividends.

- Check Schedules CYLA, BFLA and CFL – this is where current-year losses set off and prior-year losses come forward. Verify your F&O loss appears in CFL if you are carrying it forward.

- Review the tax computation, pay any balance tax via Challan 280 (self-assessment tax), and submit.

- e-Verify within 30 days – Aadhaar OTP is fastest. Our guide on e-verification of ITR covers every method. Then track your refund status.

Reporting F&O losses: your most valuable tax asset

An F&O loss is a non-speculative business loss:

- Same year: set it off against any head of income except salary – rental income, interest, capital gains, other business income.

- Carry forward: the unabsorbed loss carries forward for 8 assessment years, usable against any business income in later years.

- The catch: carry-forward is available only if you file by the Section 139(1) due date – 31 August 2026 for non-audit ITR-3 filers. A belated return permanently forfeits the carry-forward.

Intraday (speculative) losses are more restricted: they set off only against speculative profits and carry forward for just 4 years. One more reason the separate disclosure matters. Also consider tax-loss harvesting for your delivery portfolio before 31 March.

Expenses F&O traders can claim

| Expense | Notes |

|---|---|

| Brokerage and exchange charges | Transaction charges, SEBI fees, stamp duty, GST on brokerage |

| Securities Transaction Tax (STT) | Fully deductible as business expense (0.02% futures / 0.1% options sell-side since Oct 2024) |

| Internet, phone, electricity | Proportion used for trading |

| Data, software and advisory | Charting tools, algo platforms, research subscriptions, courses |

| Depreciation | Laptop/computer at 40%, furniture at 10% |

| Professional fees | CA fees for accounting, audit and return filing |

| Interest on borrowed capital | If you borrowed funds used for trading margin |

Only genuine, documented, trading-related expenses qualify. Personal expenses claimed as business expenses are a common notice trigger.

Advance tax for F&O traders

If your estimated tax liability is Rs 10,000 or more, advance tax applies:

| Instalment | Due date | Cumulative tax payable |

|---|---|---|

| 1st | 15 June 2025 | 15% |

| 2nd | 15 September 2025 | 45% |

| 3rd | 15 December 2025 | 75% |

| 4th | 15 March 2026 | 100% |

Shortfalls attract interest under Sections 234B and 234C. Because trading income is volatile, re-estimate each quarter. Traders under 44AD may pay the entire amount in one instalment by 15 March.

New vs old tax regime for F&O traders

F&O profit is taxed at your normal slab rates in both regimes – business expenses are deductible in both. The difference is in the slabs and other deductions:

- New regime (default): zero tax up to Rs 12 lakh of taxable income thanks to the Section 87A rebate of Rs 60,000 – and since F&O income is slab income (not a special-rate income), the rebate applies to it. See the full income tax slabs for FY 2025-26 and our new tax regime guide.

- Old regime: worth it only if your 80C/80D/HRA-type deductions are large. Remember the one-time-switch rule for business income (Form 10-IEA).

Note: your FY 2025-26 return is still filed under the Income-tax Act, 1961. The new Income Tax Act 2025 applies to income earned from 1 April 2026 onwards.

ITR due dates for AY 2026-27 – what changed

| Category | Due date |

|---|---|

| Salaried / no business income (ITR-1, ITR-2) | 31 July 2026 |

| F&O traders – ITR-3/ITR-4, no audit | 31 August 2026 (new – Finance Act 2026) |

| Tax audit cases | 31 October 2026 |

| Belated / revised return | 31 December 2026 |

The Finance Act 2026 permanently moved the non-audit ITR-3/ITR-4 due date from 31 July to 31 August. Do not rely on the extra month, though – file early, because a belated return means a late fee up to Rs 5,000 and loss of carry-forward.

Common mistakes that trigger tax notices

- Not filing at all because “I only made losses” – your F&O turnover is reported in AIS; non-filing invites a notice, and you lose the loss carry-forward.

- Using ITR-1 or ITR-2 despite F&O trades – wrong form means a defective return.

- Clubbing intraday with F&O – now expressly separate fields in ITR-3.

- ITR not matching AIS/broker data – always reconcile all brokers’ statements with AIS.

- Claiming personal expenses as trading expenses without documentation.

- Missing advance tax instalments and getting 234B/234C interest.

- Missing the due date and permanently losing the 8-year carry-forward.

- Ignoring the balance sheet – unexplained capital jumps invite scrutiny.

How to fill the Balance Sheet and Trading Account in ITR-3 for F&O

This is the part of ITR-3 that stops most traders, and the schedule where mistakes most often turn into a defective-return notice. You do not need audited accounts to complete it — your broker statements and bank statements contain everything required.

Where the figures come from

| ITR-3 field | Source document |

|---|---|

| Broker margin / ledger balance | Broker ledger or funds statement as on 31 March 2026 |

| Bank balance | Bank statement as on 31 March 2026 |

| Stock-in-trade | Holdings statement — only shares held as trading stock |

| Fixed assets | Your own depreciation working — laptop, furniture at written-down value |

| Gross receipts / turnover | Broker Tax P&L — absolute sum of profits and losses |

| Expenses | Broker charges ledger plus your own expense records |

Trading Account and Profit & Loss

Enter your F&O turnover as gross receipts, then deduct the expenses actually incurred. Use the dedicated F&O fields and keep intraday figures in the separate speculative fields — do not combine them.

| Line | Example |

|---|---|

| Gross receipts (F&O turnover, ICAI method) | ₹42,00,000 |

| Less: brokerage, STT, exchange and SEBI charges, GST, stamp duty | ₹1,85,000 |

| Less: internet, data and advisory subscriptions | ₹60,000 |

| Less: depreciation on laptop at 40% | ₹32,000 |

| Less: professional fees | ₹15,000 |

| Net profit / (loss) from F&O | ₹3,08,000 |

Balance Sheet — what goes where

Assets side

- Broker margin balance as on 31 March — the single figure most traders forget

- Bank balances of accounts used for trading transfers

- Cash in hand

- Fixed assets at written-down value — laptop, desk, chair used for trading

- Stock-in-trade — only if you hold shares as trading stock. Delivery shares held as investment belong in Schedule CG, not here

Liabilities and capital side

- Proprietor’s capital account — see the reconciliation below

- Loans — only where genuinely borrowed for trading margin

- Sundry creditors — typically nil for a trader

The capital account reconciliation

Your closing capital is not a number you choose. It is computed:

| Opening capital as on 1 April 2025 | ₹12,00,000 |

| Add: fresh funds introduced during the year | ₹2,00,000 |

| Add: net profit for the year | ₹3,08,000 |

| Less: withdrawals for personal use | (₹4,00,000) |

| Closing capital as on 31 March 2026 | ₹13,08,000 |

Total assets must equal capital plus liabilities. If they do not, the usual culprit is an omitted broker balance, a missed withdrawal, or funds moved between broker and bank that were counted twice.

⚠️ The mistake that triggers notices. An unexplained jump in capital between years is one of the clearest scrutiny flags there is. If your capital rose by ₹15 lakh on a declared profit of ₹3 lakh, be ready to evidence where the other ₹12 lakh came from. Record fresh introductions properly rather than letting capital simply absorb them.

If you do not maintain regular books

ITR-3 provides a short alternative for taxpayers not maintaining formal books, requiring only four figures: sundry debtors, sundry creditors, stock-in-trade and cash balance. Leaving even this blank is a common cause of a return being treated as defective under Section 139(9).

Frequently asked questions

I have salary plus F&O income. Which form?

ITR-3. It has full schedules for salary, business income, capital gains and other sources. Your employer’s Form 16 goes into Schedule S, F&O into the business schedules.

I made only an F&O loss this year. Should I still file?

Yes – emphatically. Filing by 31 August 2026 preserves the loss for set-off against profits for up to 8 years. Skipping it wastes a real tax asset and can trigger an AIS-mismatch notice.

I trade through multiple brokers. How do I report?

Add up turnover, profit/loss and expenses across all brokers and report combined figures in one ITR-3. Keep each broker’s tax P&L statement as backup.

Is tax audit needed if I have an F&O loss?

Not merely because of the loss. Audit depends on turnover (Rs 10 crore digital limit) and the 44AD conditions explained above.

What if I miss the 31 August 2026 deadline?

You can file a belated return until 31 December 2026 with a late fee up to Rs 5,000 (Rs 1,000 if income is below Rs 5 lakh) – but the F&O loss carry-forward is gone permanently. Details in our late filing penalty guide.

I trade in my spouse’s account with my money. Whose income is it?

Clubbing provisions (Section 64) can attribute that income back to you. Structure this carefully with professional advice.

Can NRIs report F&O income the same way?

The classification is the same, but residency rules and DTAA can change the outcome – see our NRI tax filing guide or speak to us.

Where do dividends from my holdings go?

Schedule OS (other sources), taxed at slab rates – not part of business income.

Get your F&O return filed by Chartered Accountants

Turnover computation, audit assessment, loss optimisation and ITR-3 filing – handled end to end by CAs who trade the markets themselves. Upload your documents to get started or contact us.

Related guides

- F&O trading profit, loss & income tax – complete FAQ

- Capital gains tax on shares and mutual funds 2026

- Income tax slabs FY 2025-26 – new vs old regime

- ITR filing for freelancers and consultants

- How to deposit self-assessment tax (Challan 280)

Disclaimer: This guide reflects the law for FY 2025-26 (AY 2026-27) under the Income-tax Act, 1961, including changes made by the Finance Act 2026, as understood in July 2026. Tax law changes frequently – consult a qualified Chartered Accountant for advice on your specific facts.