Futures & Options (F&O) trading has exploded in India, but the way profits and losses are taxed still confuses most traders. This guide answers the most common questions on F&O profit and loss calculation and how to file your income tax return (ITR) for derivatives trading, fully updated for FY 2025-26 (AY 2026-27).

1. Is F&O income business income or capital gains?

F&O income is business income (Profits & Gains from Business or Profession), not capital gains. As per Section 43(5)(d) of the Income-tax Act, trading in derivatives on a recognised stock exchange is specifically excluded from the definition of “speculative transaction.” So F&O is a non-speculative business, whether you trade full-time or alongside a salary.

2. Is F&O speculative or non-speculative income?

This is the most important distinction for traders:

- F&O (futures & options) — non-speculative business income.

- Intraday equity (cash market, no delivery) — speculative business income, taxed and set off separately.

- Delivery-based equity — usually capital gains (or business income if traded frequently).

Keep these three buckets separate in your books, because the loss set-off and carry-forward rules differ for each.

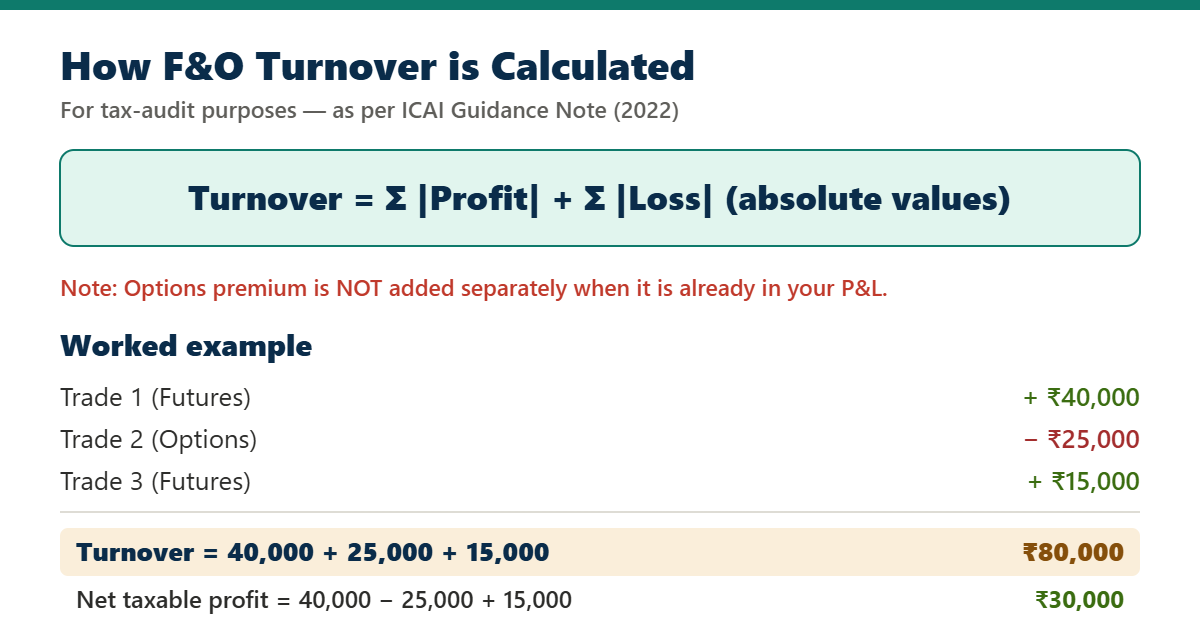

3. How is F&O turnover calculated?

For income-tax and tax-audit purposes, F&O “turnover” is not the total contract value. As per the ICAI Guidance Note on Tax Audit (2022 edition), turnover is the absolute (total) of all profits and losses from your trades — add the favourable and unfavourable differences, ignoring the plus/minus signs.

Under the current method, the premium received on sale of options is not added separately if it is already reflected in your profit and loss. Your broker’s tax/turnover statement (P&L report) usually shows this figure for you.

4. Which ITR form should an F&O trader use?

- ITR-3 — for individuals/HUFs with F&O (business) income. This is the form for most traders, and the only form that lets you carry forward losses.

- ITR-4 (Sugam) — only if you opt for presumptive taxation under Section 44AD and meet the conditions.

ITR-1 and ITR-2 cannot be used if you have F&O income.

5. How is F&O profit taxed?

F&O profit is added to your total income and taxed at your normal slab rates — there is no special flat rate. For FY 2025-26, the new tax regime is the default, with a basic exemption of ?4 lakh and a Section 87A rebate that effectively makes a taxable income of up to ?12 lakh tax-free. The old regime (basic exemption ?2.5 lakh, with deductions) remains optional.

6. What expenses can F&O traders deduct?

Because F&O is a business, you can deduct expenses incurred to earn that income, including:

- Brokerage, exchange transaction charges, SEBI and stamp charges, GST on brokerage

- Securities Transaction Tax (STT) — now allowed as a business expense

- Internet, mobile and electricity bills (business portion)

- Trading software, data/subscription and advisory fees

- Depreciation on computer/laptop, and salary paid to staff, if any

Keep invoices and proof — only genuine, trading-related expenses are allowed.

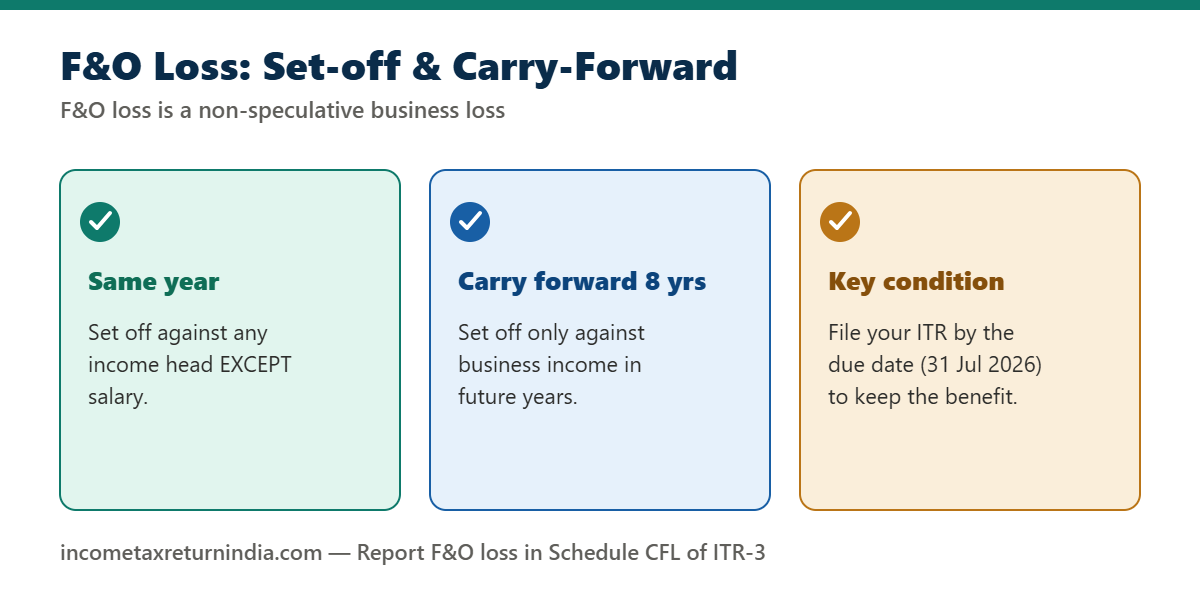

7. How are F&O losses set off and carried forward?

An F&O loss is a non-speculative business loss, which gives it flexible treatment:

- Same year: set off against income under any head except salary (e.g. rental income, interest, capital gains, other business income).

- Carry forward: any unabsorbed loss can be carried forward for 8 assessment years, but in later years it can only be set off against business income.

- Crucial condition: you must file your ITR on or before the due date (31 July 2026 for non-audit cases) and report the loss in Schedule CFL. A belated return loses the carry-forward benefit.

8. Is a tax audit mandatory for F&O trading?

A tax audit under Section 44AB is not automatically triggered just because you made a loss. It depends on turnover and whether you use presumptive taxation:

- Audit applies if F&O turnover exceeds ?1 crore. This limit rises to ?10 crore where cash receipts and cash payments are each 5% or less of the total — which covers almost all F&O traders, as trades are fully digital.

- If turnover is within ?10 crore and you are not bound by Section 44AD, no audit is required even if you have a loss.

- An audit can be triggered under Section 44AD(e) if you had opted for presumptive taxation in any of the last 5 years, now declare profit below 6%/8%, and your total income exceeds the basic exemption limit.

9. Can F&O traders use presumptive taxation (Section 44AD)?

Yes, if turnover is up to ?2 crore (?3 crore where cash is 5% or less). Under 44AD you simply declare 6% of turnover (digital) as profit, file ITR-4, and skip detailed books and audit. The trade-offs: you cannot claim actual expenses or carry forward losses, and once you opt in you are generally locked in for 5 years.

10. What changed in STT on F&O from October 2024?

From 1 October 2024, Securities Transaction Tax on F&O sales increased:

- Futures: STT on the sell side rose from 0.0125% to 0.02% of the traded price.

- Options: STT on the sell side rose from 0.0625% to 0.1% of the option premium.

This raises trading costs, but the STT you pay is deductible as a business expense.

11. Do I have to pay advance tax on F&O income?

Yes. If your total tax liability for the year is ?10,000 or more, you must pay advance tax in four instalments (15 June, 15 September, 15 December and 15 March). Missing instalments attracts interest under Sections 234B and 234C.

12. Are F&O transactions shown in AIS?

Yes. Your F&O turnover and related information now appear in the Annual Information Statement (AIS) on the income-tax portal. Always reconcile your ITR with your broker’s P&L statement and the AIS to avoid mismatches and notices.

13. What are the ITR due dates for AY 2026-27?

- 31 July 2026 — non-audit cases (most traders).

- 31 October 2026 — cases requiring a tax audit.

- A belated return can be filed up to 31 December 2026, but you lose the right to carry forward losses.

14. How to file your F&O tax return — step by step

- Download your broker’s annual P&L / tax statement for FY 2025-26.

- Compute turnover and net profit/loss, and total your trading expenses.

- Decide on the regime (new vs old) and check whether tax audit or 44AD applies.

- Report F&O under “Income from Business/Profession” in ITR-3 (keep intraday and capital gains separate).

- Pay any balance/advance tax, file before the due date, and e-verify the return.

Need help filing your F&O tax return?

Let our Chartered Accountants compute your turnover, handle the tax audit if needed, and file your ITR-3 accurately — with maximum loss benefit. Just share your details to get started.

Related income tax guides

- File your income tax return online (FY 2025-26)

- ITR filing for salaried individuals

- ITR filing for freelancers & consultants

- New tax regime FY 2025-26 explained

- Tax planning tips to save tax

Disclaimer: This page is for general information only and reflects the law as understood for FY 2025-26 (AY 2026-27). Tax rules and due dates can change or be extended. Please consult a qualified Chartered Accountant for advice on your specific situation.